Personal Finance

The UK tax year ends on 5 April 2026. After that date, your annual allowances reset, and any you haven't used simply disappear. Now is a good time to ensure that you’re making the most of your allowances and investing as tax-efficiently as possible.

Here is a checklist to help you make the most of your tax year before it ends.

1. Use Your ISA Allowance

Everyone in the UK gets a £20,000 allowance to put into an ISA each tax year. Money inside an ISA grows completely free of tax, no income tax, no Capital Gains Tax, ever. You can split it across a Cash ISA, a Stocks & Shares ISA, or both. But whatever you don't use by 5 April? Gone forever.

If you are between the ages of 18 and 39, the Lifetime ISA (LISA) lets you save up to £4,000 for your first home or retirement, and the government tops it up with a 25% bonus. That's up to £1,000 free money every year.

2. Maximising Your Pension Contributions (SIPP)

Pension contributions are one of the most powerful ways to cut your tax bill, and most people don't use anywhere near their full allowance. You can contribute up to £60,000 this tax year. And here's the kicker: the government adds tax relief on top. Put in £800, and HMRC adds £200, your pension receives £1,000. A Self-Invested Personal Pension (SIPP) is a pension you open yourself, separate from any workplace pension.

If you are a higher-rate taxpayer, you can claim even more back through your self-assessment return. If you didn't use your full allowance last year? You may be able to carry forward unused pension allowances from the past three tax years, but only after you've maxed the current year first.

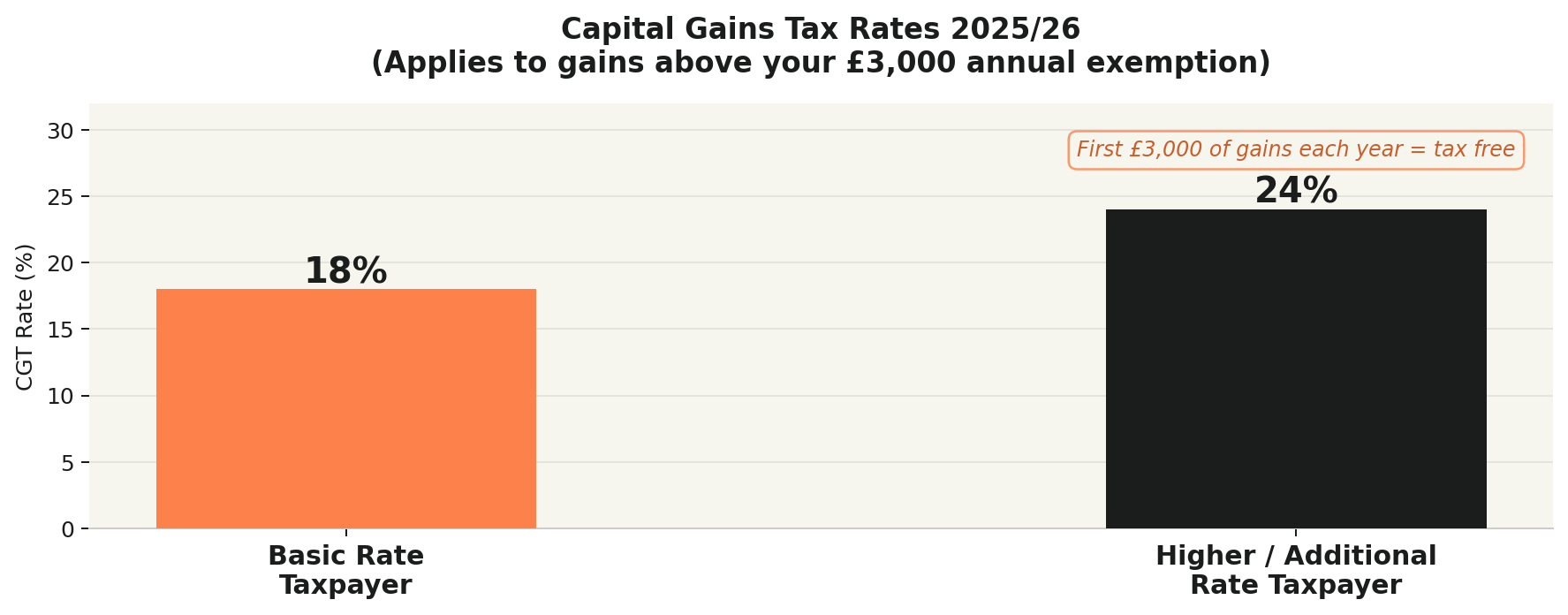

3. Check Your Capital Gains Tax Position

If you sold investments, a second property or shares this year, you may owe Capital Gains Tax (CGT). CGT is a tax on your profit, not the full sale price. You get a £3,000 annual exemption before any tax kicks in.

For example, if you were to buy a piece of art for £5,000 and later sell it for £20,000, you would have made a £15,000 gain on the asset, and you may need to pay CGT on this £15,000 sum. Assuming you’ve ‘disposed’ of no other assets in the current tax year, you would need to pay CGT on £12,000, the capital gain (£15,000) less the CGT allowance (£3,000).

The CGT rate for basic-rate taxpayers is 18%, while higher- and additional-rate taxpayers face a rate of 24%.

4. Do Not Forget Dividends

If you receive dividends from shares held outside an ISA, you only get £500 tax-free this year. Anything above that is taxed. Where possible, hold dividend-paying investments inside your ISA.

Quick Reference — Key Numbers for 2025/26

| Allowance | Amount |

|---|---|

| ISA (per adult) | £20,000 |

| Junior ISA (per child) | £9,000 |

| Lifetime ISA | £4,000 (+ 25% govt bonus) |

| Pension Annual Allowance | £60,000 |

| Capital Gains Tax exemption | £3,000 |

| Dividend allowance | £500 |

| CGT rate — basic rate taxpayer | 18% |

| CGT rate — higher rate taxpayer | 24% |

This article is for informational purposes only and is not financial advice. Tax rules vary by individual and may change. Always speak to a qualified financial adviser if you are unsure.

Questions? Drop them in the comments below.

Members Discussion