Personal Finance

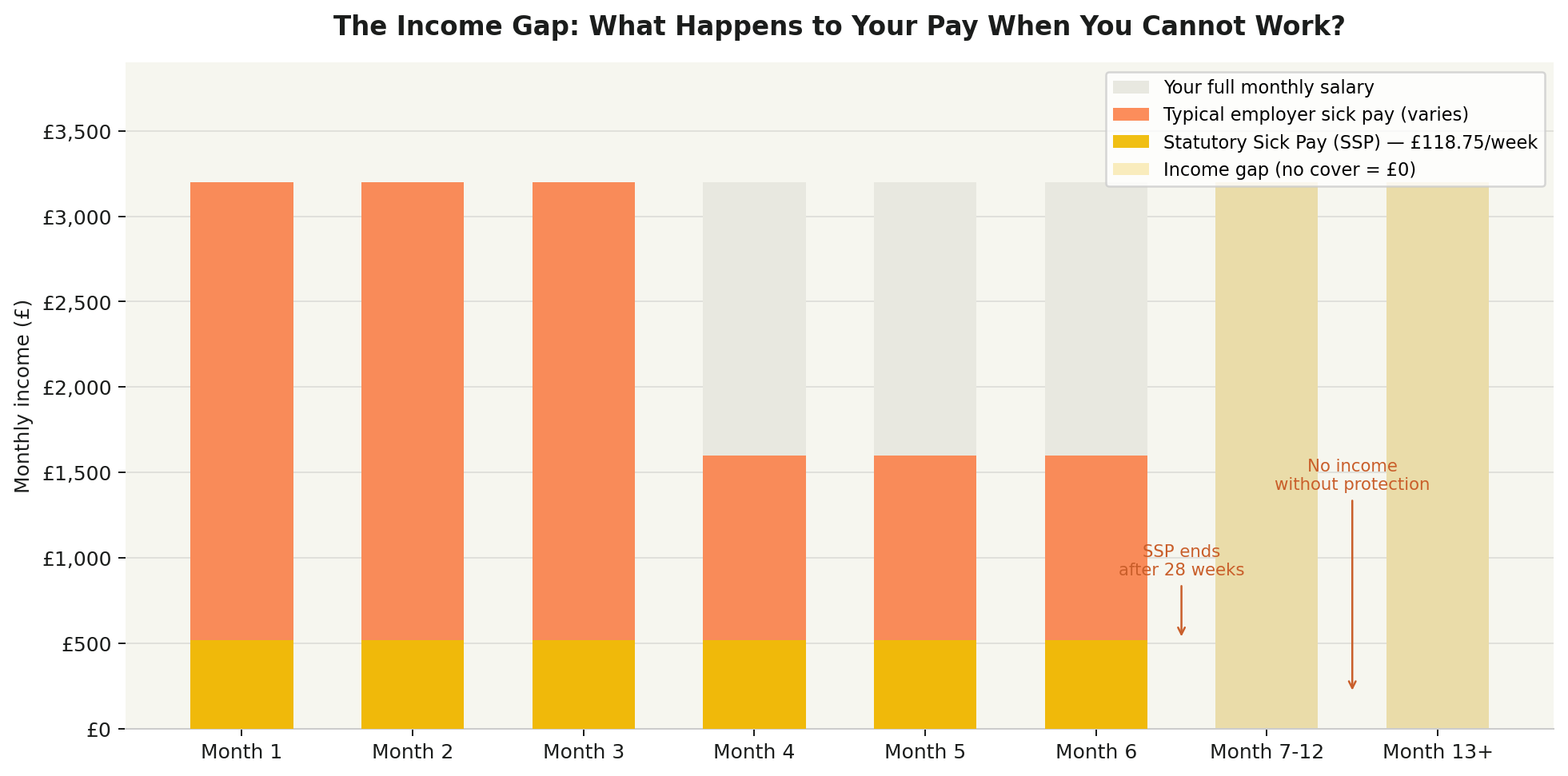

We insure our cars, our homes, and even our phones. Yet very few of us insure the one thing that pays for all of those things, our income. If illness or injury stopped you from working tomorrow, how long could you last on your savings before things got difficult? For most people in the UK, the honest answer is, not very long. It's worth noting that the current statutory sick pay is £118.75 per week, usually paid by the employer for up to 28 weeks. Income protection insurance exists to fill that gap.

It is, in essence, a replacement wage if you're unable to work because of illness or injury. Its monthly payouts can help you stay buoyant through turbulent times, so you can focus on getting better and back to work.

To understand why this matters, consider what actually happens to your income when you are too ill to work. In the first weeks, your employer's sick pay kicks in if they offer any above the legal minimum. Many employers pay full salary for one to three months, then half salary for another three. But after six months, most employees are receiving nothing beyond statutory sick pay (SSP). After 28 weeks, SSP stops too.

The chart above tells the story plainly. The income gap, the distance between what you were earning and what you actually receive, can open wide and fast. Mortgage, rent, utility bills, and food costs wait for no one. If James, a marketing manager, earns £3,333 per month after tax and is diagnosed with a serious back condition and cannot work. His employer pays full salary for three months, then half salary for three months. By month seven, he is receiving only SSP £515 per month. His mortgage alone is £1,100. Without income protection, James begins drawing on savings and, within months, faces serious financial difficulty.

Some companies include this in their contract, typically stating a coverage amount (e.g 50 - 80 % of an employee’s salary), deferred period, rehabilitation support, etc. Alternatively, or in addition to the coverage provided by your employer, you can get coverage by making monthly contributions. So how does income protection work?

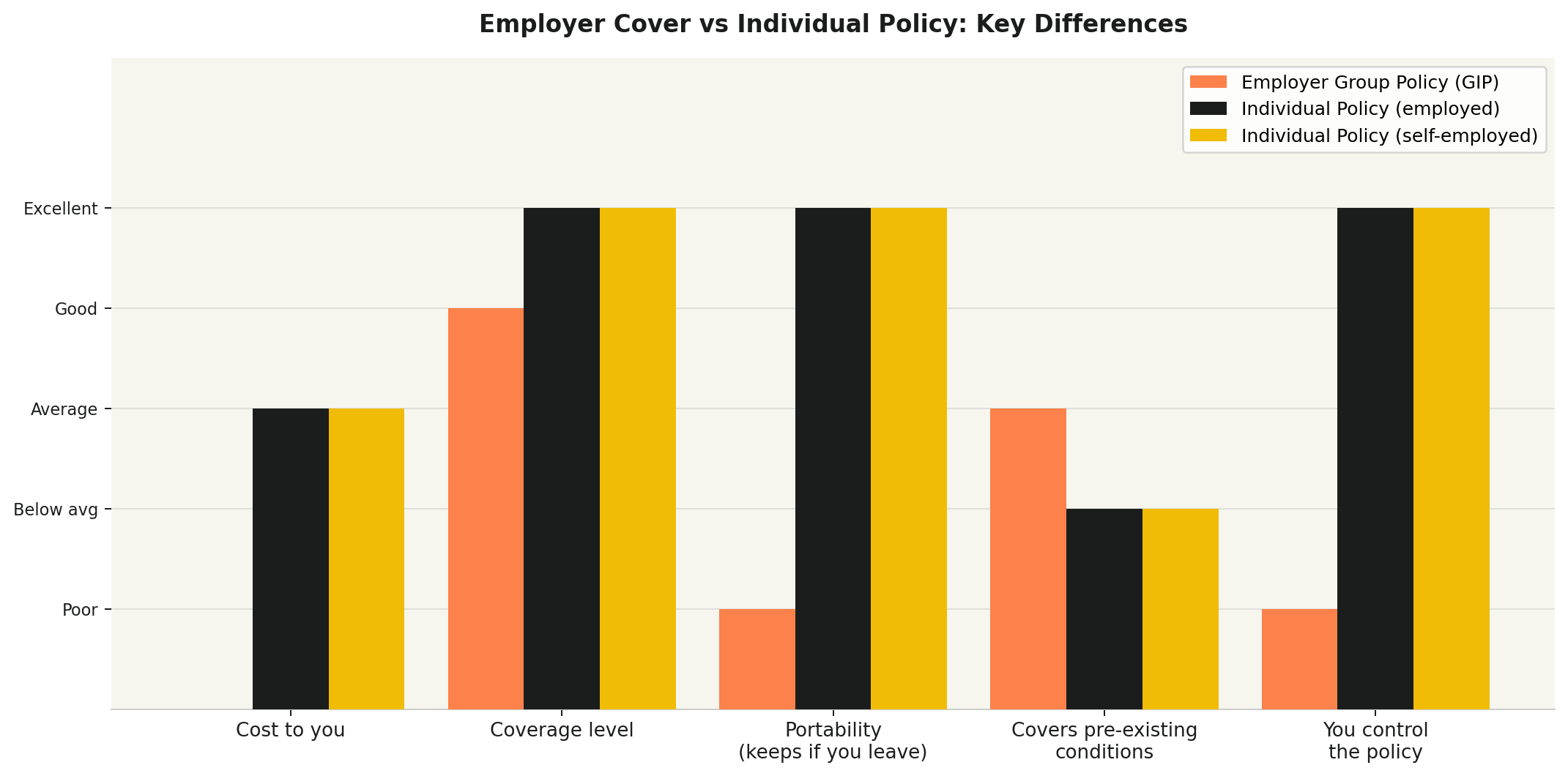

Many people have income protection through their employer without realising it. It is often buried in your employment contract or benefits handbook under the term Group Income Protection (GIP).

Here is exactly how to check:

- First, review your employment contract and search for phrases such as income protection, group income protection, long-term sickness benefit, or permanent health insurance (PHI).

- Second, log in to your company's employee benefits portal, where all your benefits are listed in one place.

- Third, email your HR department directly. A simple message asking "Does the company provide group income protection insurance, and if so, what is the deferred period and coverage level?" will get you the answer quickly.

- Fourth, check your payslip.

What your contract will typically say

If your employer does provide it, your contract will usually specify three things: the coverage level (most commonly 50% to 75% of your salary), the deferred period (how long you must be off sick before payments begin typically 13, 26, or 52 weeks), and whether the benefit is linked to the company's own definition of incapacity or an insurer's definition.

For example, Sarah's contract states that "Employees who have completed their probationary period are entitled to Group Income Protection at 66% of basic salary, after a deferred period of 26 weeks." This means if Sarah is off sick for more than 26 weeks, the policy will pay her 66% of her salary, roughly £1,980 per month on a £36,000 salary, for as long as she cannot work, up to the policy's maximum term.

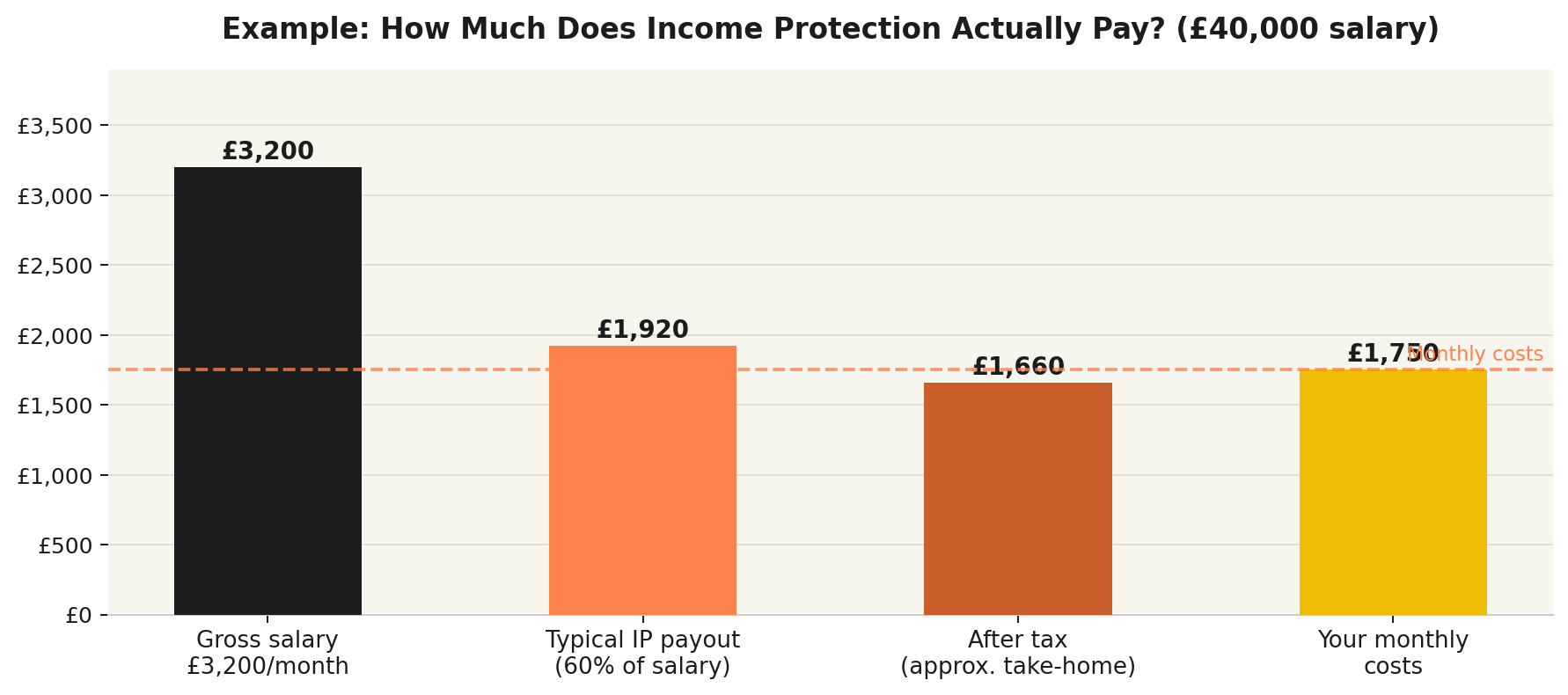

Employer Group Income Protection typically covers 50% to 75% of your gross salary. Income protection payouts from employer policies are taxed as income because your employer pays the premiums. On a £40,000 salary, a 60% payout of £2,000 per month becomes roughly £1,660 after basic rate tax. If your monthly committed costs, mortgage, bills, food, travel, are £1,750, you are already short.

How to calculate your shortfall

- Find your monthly take-home salary (after tax and National Insurance).

- Identify your essential monthly outgoings, like mortgage or rent, council tax, utilities, food, minimum debt payments, and any other non-negotiable costs.

- Check your employer's coverage level and deferred period.

- Calculate what 50–75% of your gross salary is, then estimate the tax you would pay on it.

- The gap between that figure and your essential outgoings is your coverage shortfall, the amount an individual policy needs to fill.

A simple rule of thumb is that if your essential monthly costs exceed 55% of your gross monthly salary, you likely need additional cover beyond what most employer policies provide.

The Deferred Period: Choosing the Right Waiting Time

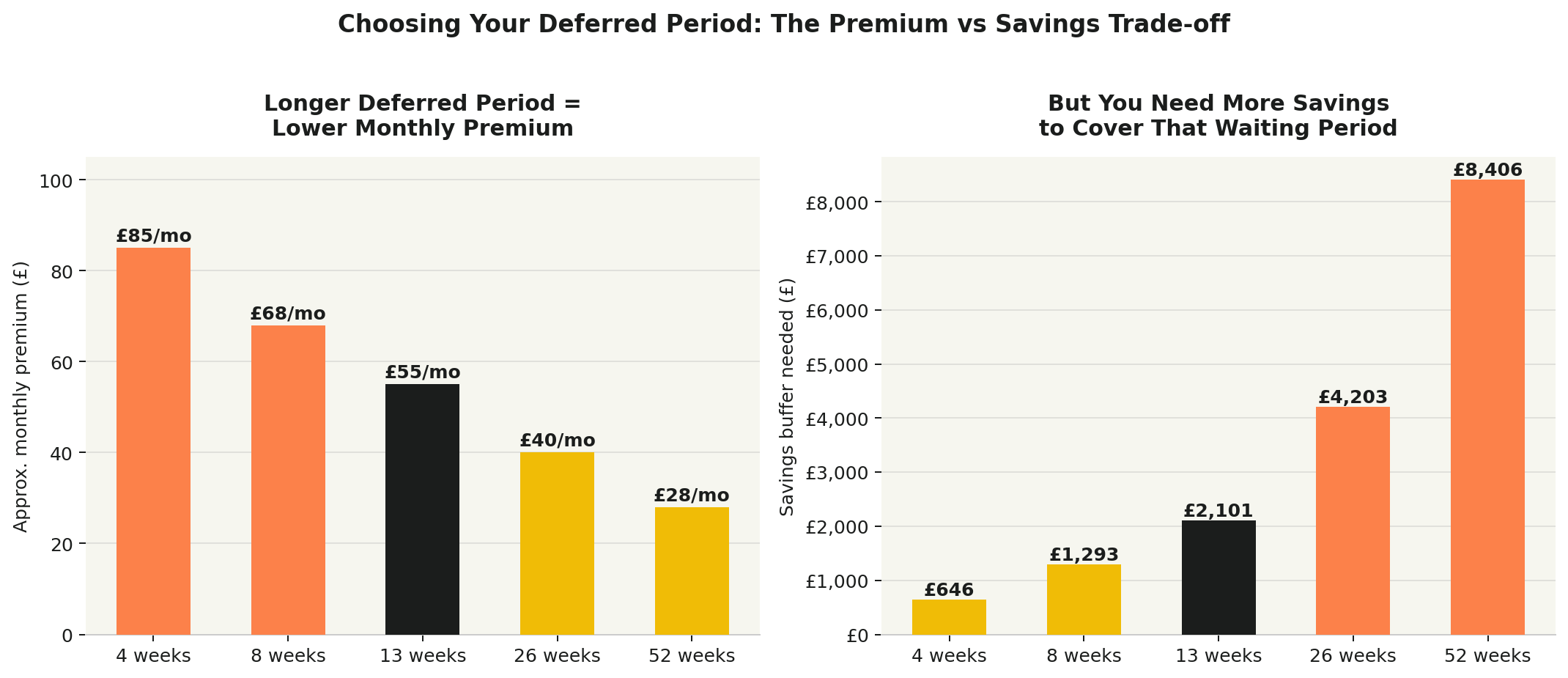

The deferred period is the gap between becoming ill and your income protection payments beginning. It is one of the most important decisions in structuring any policy, and it directly affects what you pay every month.

A shorter deferred period means higher monthly premiums, but you need fewer savings to survive the wait. A longer deferred period means lower premiums, but you must have enough in savings to cover that gap yourself.

The sweet spot for most people is aligning the deferred period with their employer's sick pay. If your employer pays full salary for three months (13 weeks), choosing a 13-week deferred period means your insurance picks up exactly where your employer's sick pay leaves off, with no gap and no overlap.

Individual Income Protection: How It Works

If your employer does not provide cover, or you want to top up what they offer, you can take out an individual income protection policy. Here is how it works.

You choose a monthly benefit, the amount you want to receive if you cannot work. Most insurers cap this at around 60% to 70% of your pre-tax income, to ensure you still have an incentive to return to work. You also choose your deferred period, the policy term (how long it will pay out some pay until a set age, such as 60 or 65, or for a fixed period, such as two or five years), and whether the benefit is level or index-linked (rising with inflation each year).

Own Occupation vs Any Occupation

This is the most important term in any income protection policy. "Own occupation" cover, pays out if you cannot perform your specific job. "Any occupation" cover, pays out if you cannot do any work at all. A surgeon with a hand injury might be unable to perform surgery but could technically work a desk job. Under any-occupation cover, they may receive nothing.

What affects your premium

Your monthly premium is calculated based on your age, your occupation, your health history, the benefit amount you choose, and the deferred period and policy term you select.

Key Questions to Ask Before Buying

Before purchasing any income protection policy, make sure you can answer the following: Does it cover your own occupation, or any occupation? What is the exact deferred period, and does it align with your sick pay? Does the benefit rise with inflation? Does it pay until retirement or only for a fixed term? What illnesses or conditions are excluded, particularly any pre-existing ones? Is the premium guaranteed, or can the insurer increase it?

A good independent financial adviser or protection specialist can model the right structure for your specific situation.

Members Discussion