Work & Career

Student loans have sparked serious debate across the UK media, parliament, and society at large. There are concerns from several quarters about the impact of student loans on graduates. This prompted Kemi Badenoch, the leader of the Conservative Party, to highlight that the system was at "breaking point" during PMQs.

How did we get here?

Before 1998, university in England was free. Then the government introduced tuition fees of £1,000 per year. In 2006, fees tripled to £3,000 and in 2012, the cap shot up to £9,000 a year. This meant that students suddenly needed to borrow tens of thousands of pounds just to get a degree.

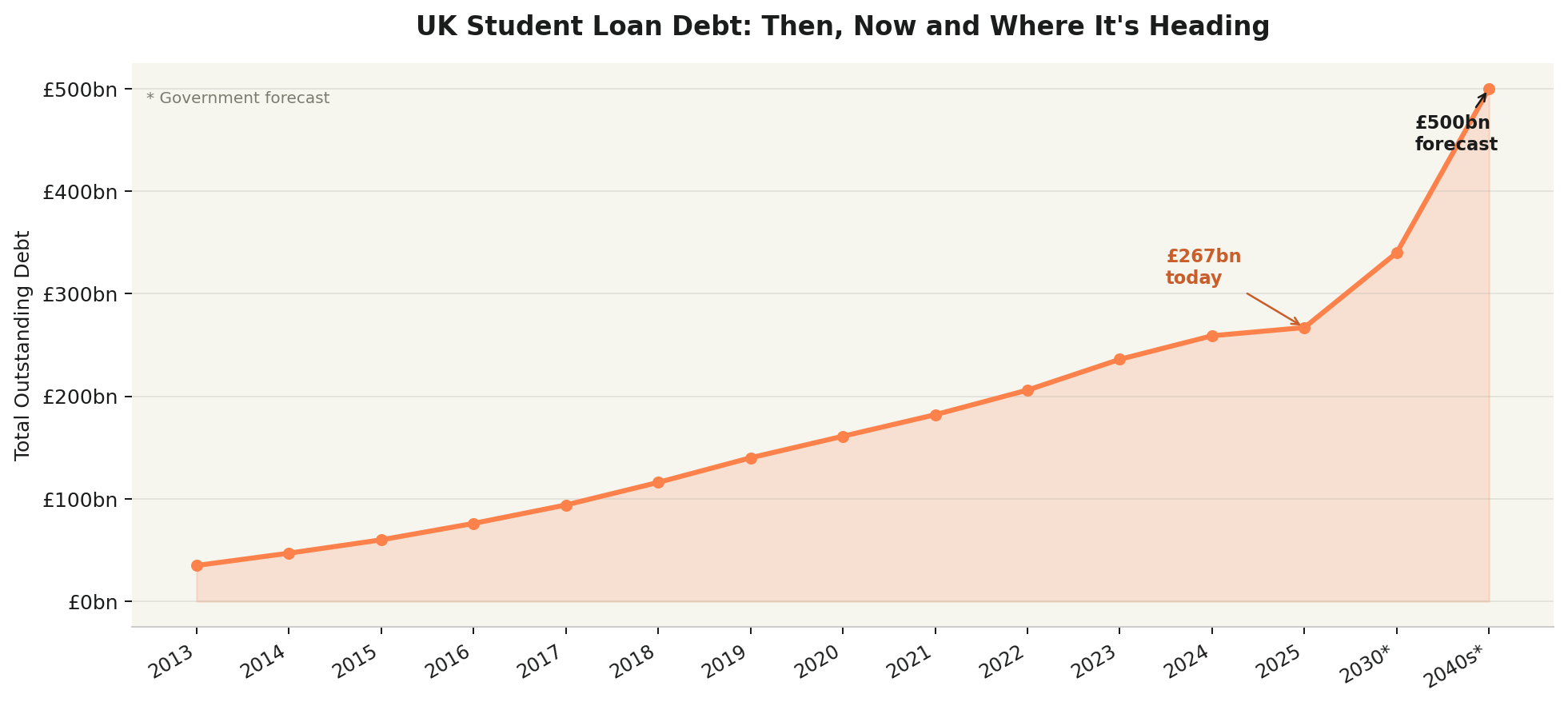

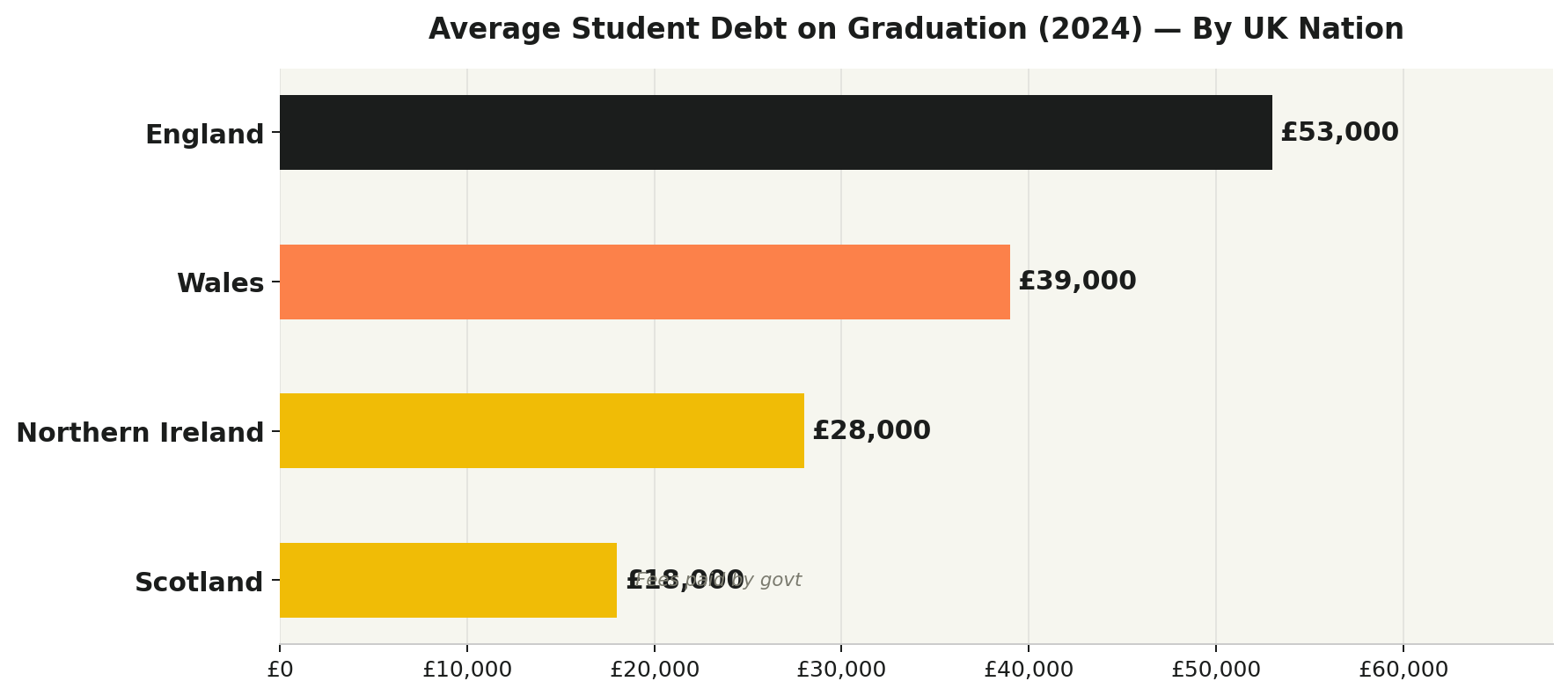

This student loan debt has been rising ever since and has hit £267 billion in March 2025, according to the House of Commons Library. The average English graduate now leaves university owing £53,000, according to the Student Loans Company (SLC) and analysis from the House of Commons Library.

The government's own forecasts put the total at £500 billion by the late 2040s

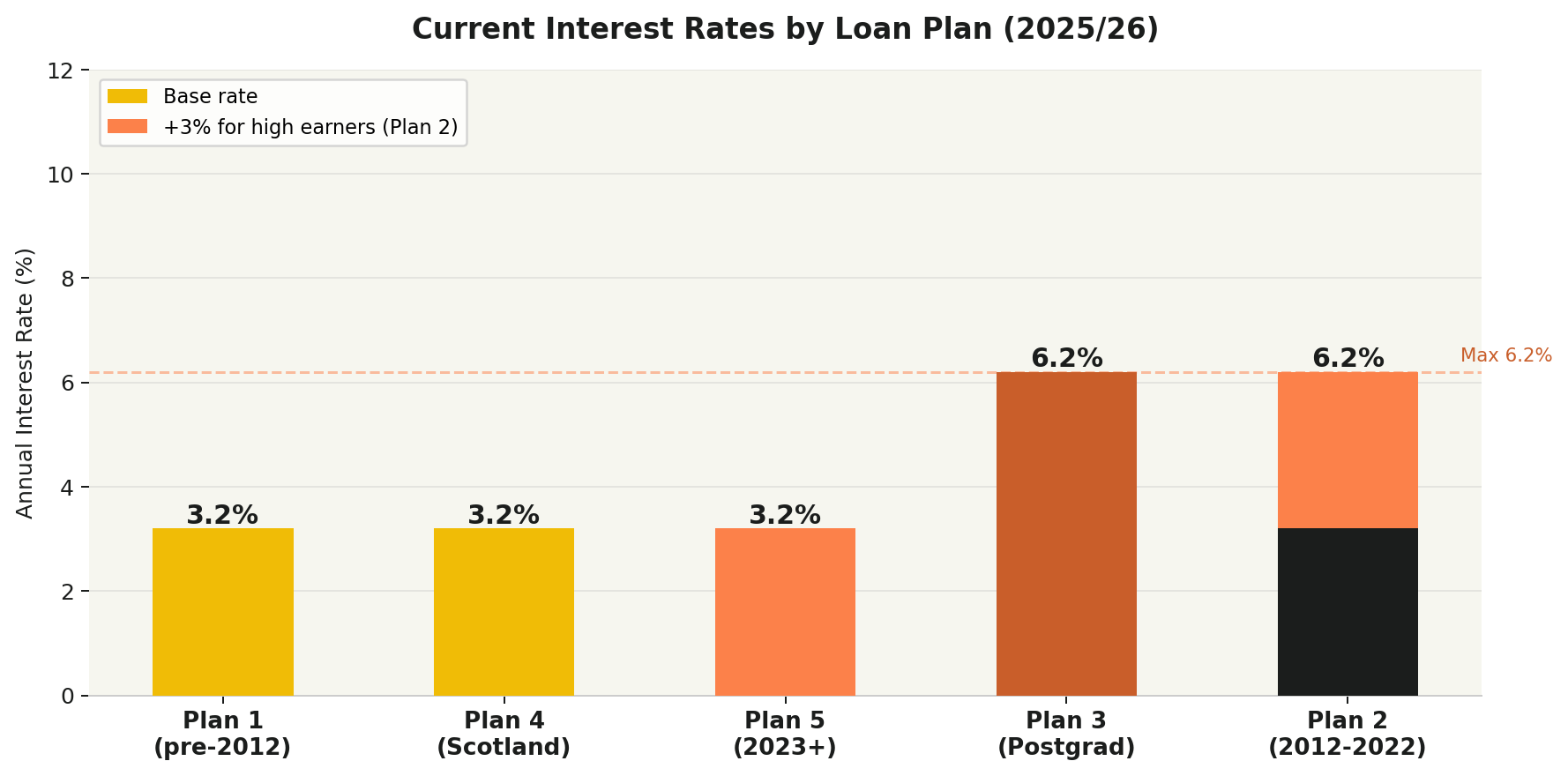

You'll be forgiven if you do not understand the student loan system; a lot of us don't. How it works, however, is dependent on when you started university. Each plan has different rules on interest rates, repayment thresholds, and the time before the debt is wiped out.

Plan 1 started before 2012, with low debt and low interest rates, and most of these graduates have already paid off their loans. Plan 2 began in 2012 up until 2022. This, however, is where the pain is. Around 4.5 million graduates are on this plan. It has higher interest rates and a thirty-year repayment period, with the debt often growing faster than you can repay it.

Plan 3 loans are taken out for master’s or doctoral courses by borrowers in England and Wales, while Plan 4 loans are for borrowers in Scotland.

Plan 5 commenced in 2023 with lower interest rates and a 40-year repayment period.

How have interest rates made it worse?

Plan 2 loans charge interest at the Retail Price Index (RPI) rate of inflation, plus up to 3% on top, depending on your salary. When inflation spiked in 2022 and 2023, the interest on student loans went through the roof. At its peak, the rate would have hit 16.5% without a government cap. Even with the cap, rates hit 8%.

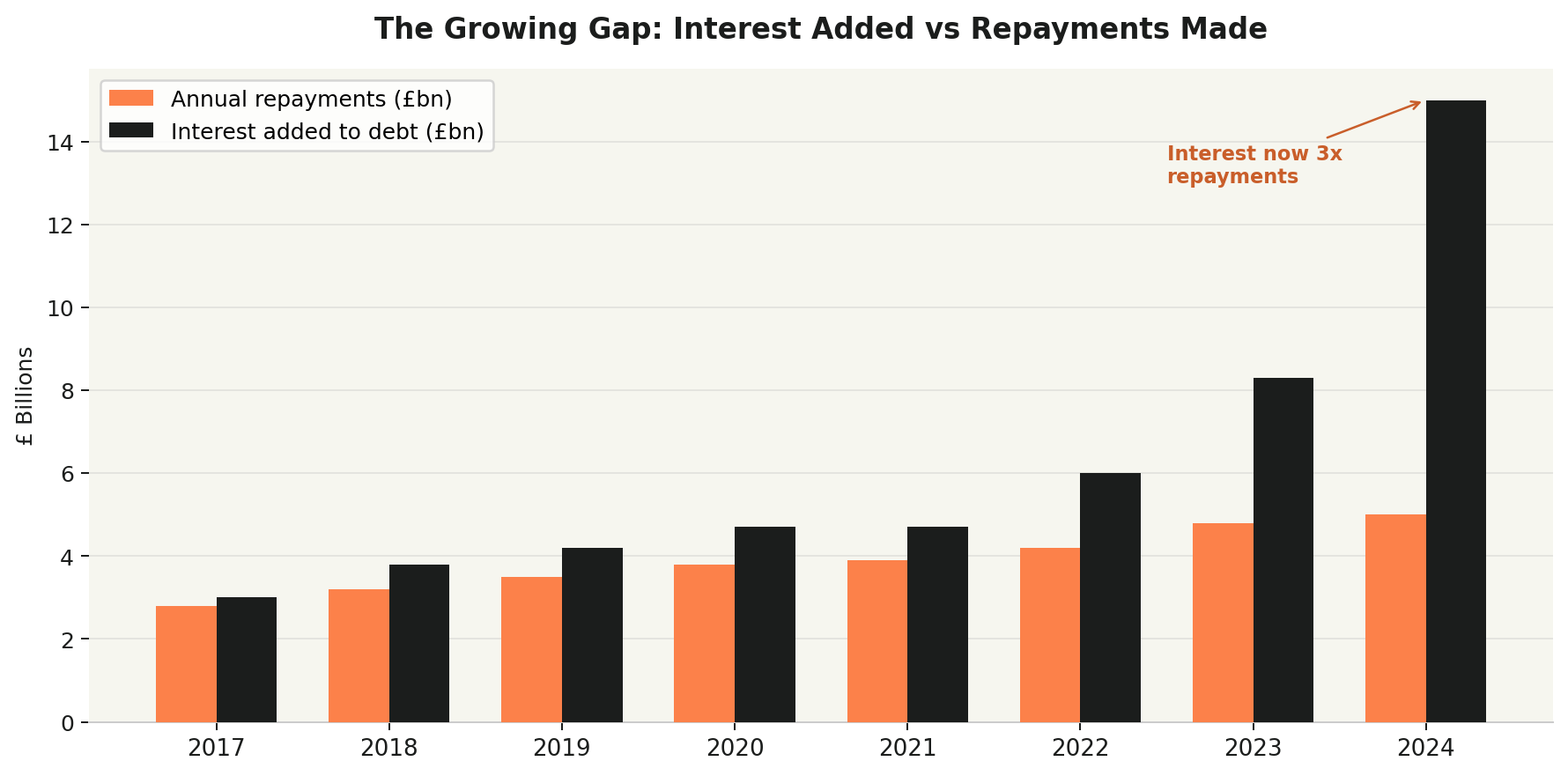

In 2024, interest added to the total loan book was £15 billion, more than three times the amount graduates actually repaid.

Why young people are struggling right now

The debt grows faster than salaries. Graduate salaries have not kept pace with the cost of living, interest rates, or loan balances. Research from Loughborough University found a gap of £8,405 per year between what students receive in maintenance loans and the cost of a basic standard of living. 67% of students surveyed said they skip meals regularly.

The repayment threshold is being frozen. The government announced in Budget 2025 that the Plan 2 repayment threshold will be frozen at £29,385 for three years from April 2027 (HM Treasury Budget 2025). This means more graduates will be dragged into repayments earlier, paying on average £3,000 more over their lifetimes.

Some graduates are paying 51% of their marginal income to the government. A Plan 2 graduate earning above £50,000 pays income tax, National Insurance, and student loan repayments combined, taking 51p of every extra pound they earn above that threshold.

What the Experts Are Saying

Martin Lewis, founder of MoneySavingExpert, has been one of the loudest critics. He called the interest rate system "not moral" and said that high inflation had left Plan 2 graduates with balances far larger than they were ever promised (Yahoo Finance UK).

The Institute for Fiscal Studies (IFS) describes student loans as functioning more like a graduate tax than a real loan for most borrowers, with repayments of 9% of income above the threshold for decades, regardless of whether the balance falls. The IFS estimates that only around 27% of graduates will ever repay in full (Institute for Fiscal Studies).

The Higher Education Policy Institute (HEPI) published a stark assessment in February 2026, saying there are only three ways to fix the crisis: cancel debt (unaffordable), lower interest rates (unwise for public finances), or make graduates repay more and faster (unpalatable). Their conclusion: all three options are unfair in different ways (HEPI, February 2026).

Some campaigners and university unions go further, arguing the loan system should be scrapped entirely and replaced with a proper graduate tax. The University and College Union has proposed a Business Education Tax on employers, arguing that companies that benefit from graduates should contribute more (Yahoo Finance UK).

Health Secretary Wes Streeting conceded publicly that "a debate on the system is worth having," even as Chancellor Rachel Reeves maintained it was "fair and reasonable" (Yahoo Finance UK). That split within government suggests reform may eventually come, but few experts expect it to come quickly.

Until interest rates are structurally reformed or the system is fundamentally redesigned, the £267 billion number will only keep climbing.

Quick Facts

| Total UK student debt (2025) | £267 billion (House of Commons Library) |

| Forecast by late 2040s | £500 billion (Dept for Education) |

| Average English graduate debt | £53,000 (Student Loans Company) |

| Plan 2 max interest rate | 6.2% (House of Commons Library) |

| Interest added in 2024 | £15 billion (House of Commons Library) |

| Repayments made in 2024 | £5 billion (Student Loans Company) |

| Graduates who repaid in full (2024) | 2,943 (Student Loan Calculator UK) |

| Graduates who repaid in full (2016) | 50,165 (Student Loan Calculator UK) |

Members Discussion