Personal Finance

You are probably among those people who have never really thought about what happens to your money if a financial institution (be it your bank, building society, or credit union) goes down, because of how stable it has been.

The truth is, this has happened before. In 2008, Northern Rock collapsed, and savers panicked. In 2023, Silicon Valley Bank failed. Should this happen, however, what happens to your money? This is where the Financial Services Compensation Scheme (FSCS) comes in.

The FSCS is the UK’s independent, free deposit guarantee scheme that automatically protects up to £120,000 per person (£240,000 for joint accounts) per authorised institution if a bank, building society, or credit union fails. This increased limit applies to deposits, savings, and cash ISAs as of 1 December 2025.

What does this mean for your money??

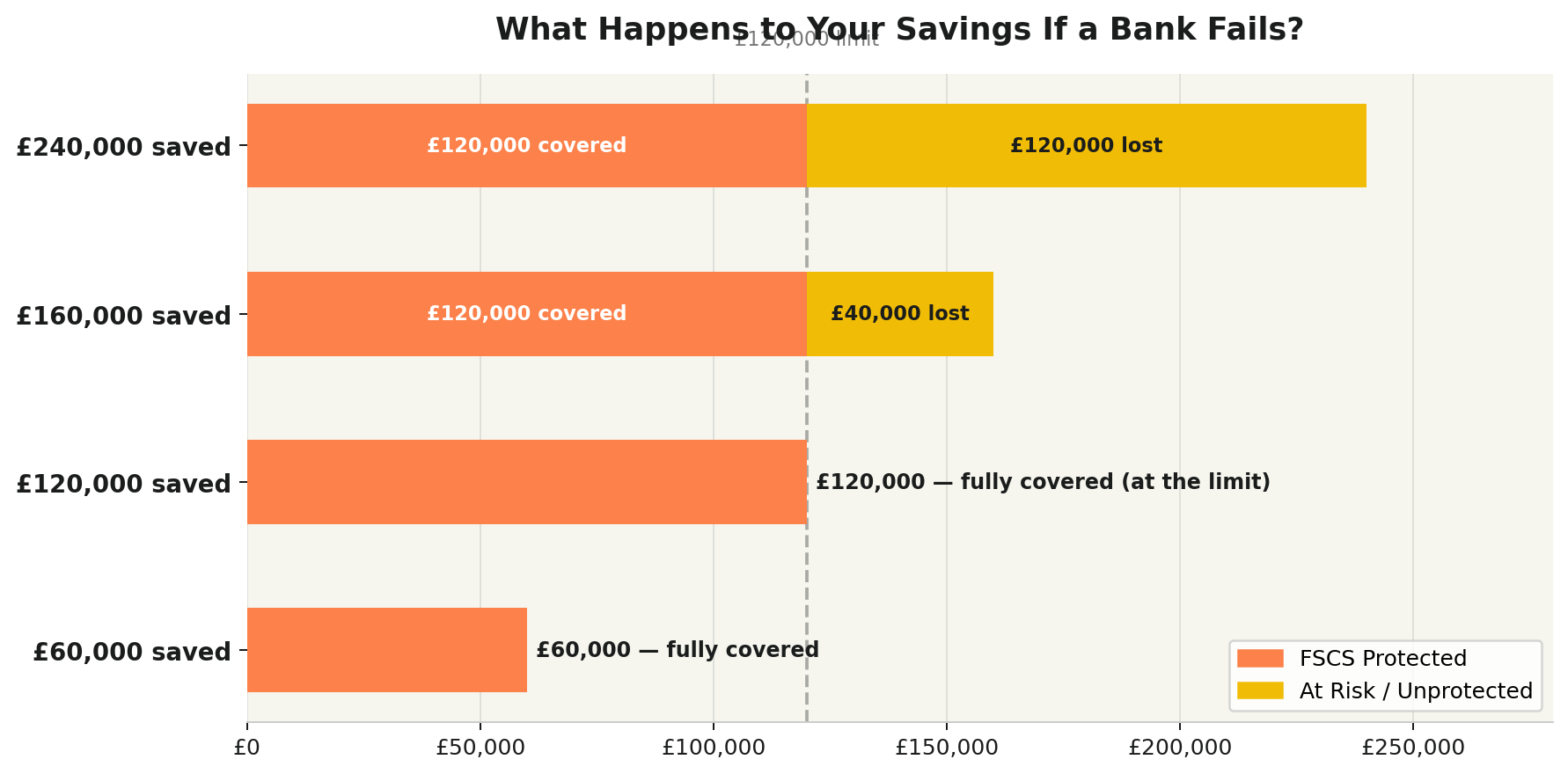

The £120,000 Coverage Limit

The FSCS protects up to £120,000 per person, per bank. For joint accounts held by two people, that doubles to £240,000. Think of it like a safety umbrella. If you're standing under it, you're protected up to the limit. Any money beyond that limit is outside the umbrella and could be lost if your bank fails.

If Sofie has been saving for years and has £150,000 in a savings account at Bank A, and it suddenly collapses, the FSCS will return £120,000 to her, but the remaining £30,000 is not covered and could be lost forever.

If you have more than £120,000 in savings, it's wise to split it across different, separately licensed banks. Each gives you a fresh £120,000 of protection.

One thing to consider here however is that some banks share a licence (e.g., HSBC/First Direct), meaning the £120,000 limit applies to the total across both, not to each.

Insurance: What's Covered and How Much?

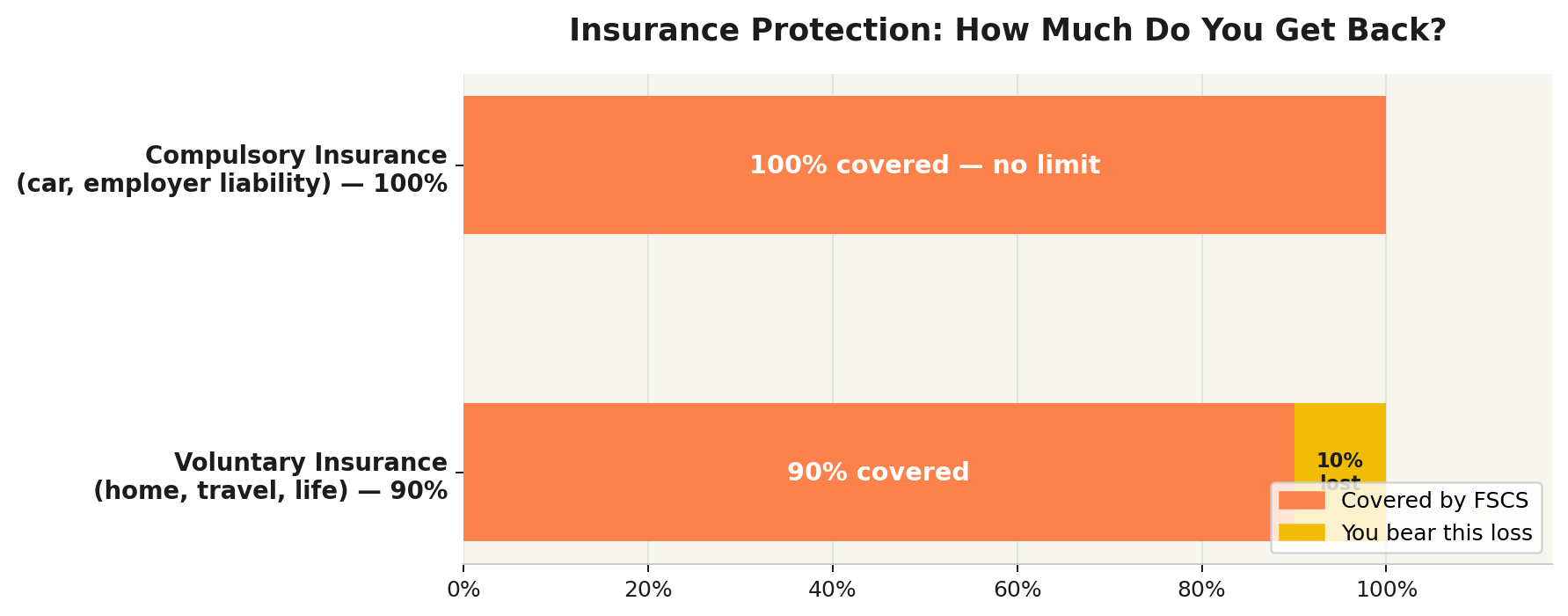

The FSCS also protects you if an insurance company fails. There are two levels of protection depending on the type of insurance.

Compulsory insurance (e.g. car insurance): By law, you must have it. If your insurer collapses, your claim is paid in full 100%, with no upper limit.

Voluntary insurance (e.g. home, travel, life): You chose to buy it. If your insurer collapses, 90% of your valid claim is paid and you bear the remaining 10%.

If David's insurer owes him £15,000 after his car was written off and before payment, the insurance company goes bust, because car insurance is compulsory, the FSCS pays David the full £15,000. Not a penny lost. If Priya, however, is owed £5,000 from her travel insurer after she cancelled her holiday due to illness and her insurer collapses, because travel insurance is optional, the FSCS pays 90% (£4,500) and Priya loses £500.

Temporary High Balances: Up to £1 Million Protection

Perhaps you sell your house, receive an inheritance, or get a legal compensation payout. These are called "Temporary High Balances", and the FSCS recognises that you shouldn't be penalised for having extra money temporarily in your account.In these situations, you can be protected for up to £1,000,000, but only for 6 months from the date the money arrives in your account.

Qualifying life events include: selling a property, receiving an inheritance, receiving a court compensation award, a divorce or separation settlement, and redundancy payouts. If Maria sells her flat for £450,000 and puts the money in her bank account while she looks for a new home, normally only £120,000 would be protected but because this is a temporary high balance from a property sale, the full £450,000 is protected for 6 months. If Maria hasn't bought her new home after 6 months, she should move any amount over £120,000 into different accounts. The 6-month window starts from the date the money arrives in your account not from when you decide to move it.

Annuities: 100% Protection, No Cap

If you buy an annuity (this is a financial product you buy usually at retirement that pays you a guaranteed income for the rest of your life. Think of it like this, you pay a company £100,000 today, and in return they promise to pay you £500 every month for as long as you live, even if you live to 105), the FSCS gives the strongest possible protection, 100% coverage with no upper limit. If Margaret used her £180,000 pension pot to buy an annuity paying her £900 a month for life. Ten years later, her annuity provider collapses, the FSCS steps in and continues paying her the full £900 a month; she loses nothing, even though £180,000 is far above the usual savings limit.

Do I need to do anything to ensure I am covered??

The simple answer is no; compensation is usually paid automatically if a firm collapses. You don't need to register, fill in a form, or pay a fee. Here's what happens if a bank fails:

- The bank is declared in default by the regulator.

- The FSCS automatically works with the failed firm to identify all customers.

- The FSCS writes to you directly, you don't need to chase them.

- Compensation is usually paid within 7 working days for deposits.

You can check if your provider (i.e., where you keep your money e.g banks, building societies, credit unions) and money are protected by checking the website.

Common Questions

Is my cash ISA protected? Yes! Cash ISAs are treated as deposits and are covered up to £120,000 per person per institution.

Does this apply to business accounts? Yes, most small businesses are covered up to £120,000. Very large businesses above certain size thresholds may not qualify.

What if I have multiple accounts at the same bank? The £120,000 limit applies to your total deposits at that bank not per account. So £60,000 in a current account and £80,000 in a savings account at the same bank means only £120,000 of the £140,000 is protected.

Is my stocks and shares ISA or pension covered? Investments are covered up to £85,000 if a firm goes bust and your assets are lost due to fraud or bad advice. This does not protect against normal market losses (when investments fall in value).

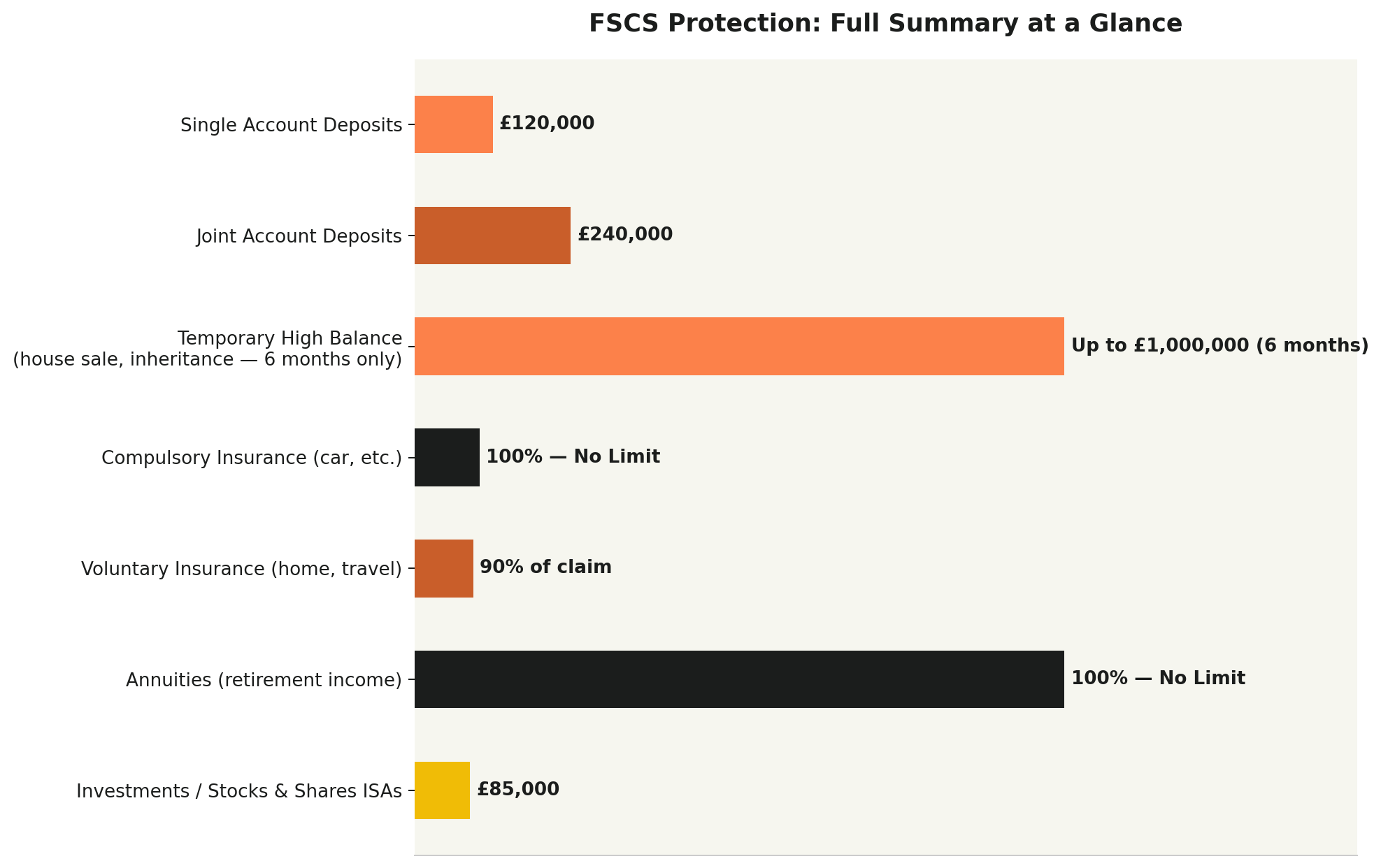

Quick Reference Table

| Product Type | Coverage | Key Detail |

|---|---|---|

| Bank / savings deposits | £120,000 | Per person, per bank |

| Joint account | £240,000 | £120,000 per person |

| Temporary High Balance | Up to £1,000,000 | 6 months only |

| Compulsory insurance | 100% — no limit | Car, employer liability |

| Voluntary insurance | 90% of claim | Home, travel, life |

| Annuities | 100% — no limit | Full retirement income protected |

| Investments / S&S ISAs | £85,000 | Fraud/firm failure only |

This article is for informational purposes only and does not constitute financial advice. Limits and rules are accurate as of the time of writing.

Do you have further questions or thoughts about your deposit protection? You can tell us in the comments.

Members Discussion